It’s been a while since I’ve posted on this blog since I have had other priorities. I read 2 books in August and gave myself permission to quit 2 other books – a true act of self-care. Previously, I didn’t allow myself to not finish books. Here is a blurb of each of the books I read in August.

“The Ritual Effect: Unlocking the Extraordinary Power of the Ordinary” was written by Michael Norton, professor of Business Administration at Harvard Business School. Here are some main takeaways:

The essence of habit is the what – something we do – brush our teeth, go to the gym, pay bills, etc. The essence of ritual is the how. It matters to us not simply that we complete the action but the specific way that we complete it. When rituals are disrupted, people report feeling “off” all day.

Some rituals become so intricate that the ritual interferes instead of prepares. Ex: performance rituals – baseball players engage in an average of 83 movements when batting.

Rituals and repetition can be powerful tools for honing our self-control, but ritualistic behavior can, over time, start to control us instead. Among the most common treatments for compulsive behaviors is “habit reversal” training – identifying the root behavior that’s causing problems and replacing it with something else.

The 4 Lessons of Relationship Rituals

Rituals wake up our experience of commitment – doing things together.

Relationship rituals are exclusive.

Rituals – not routines – bring the magic.

Consensus is a critical factor. Do you and your partner agree that it’s a ritual and not just a routine?

Food and drink are often central to rituals, but how we share them is what shapes family identity.

Rituals can be the practices that call us home and bring family together.

Family rituals immerse us in the moment, strengthen identity, and create lasting meaning.

Rituals give us a sense of ownership, an affirmation of identity or belonging, or an increased feeling of meaning.

Personal rituals are more adaptable and meaningful than inherited rituals since we can shape them to fit our values and goals.

Rituals strengthen social bonds through shared meals, celebrations, or communal ceremonies.

Rituals don’t have to be complex. Simple, intentional actions can transform daily life.

4 out of 5 stars

“Crush Your Money Goals” was written by Bernadette Joy, an expert money coach and founder of CRUSH Your Money Goals. Here are some main points.

CRUSH:

Curate your accounts. Coordinate accounts and track spending.

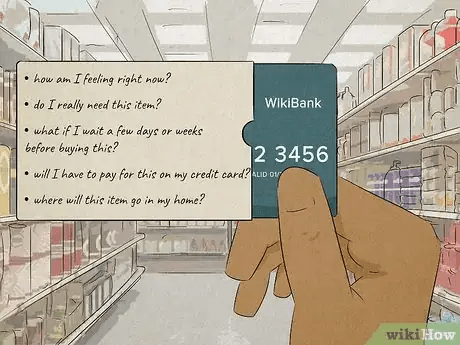

Reverse into independence. Set clear financial independence goals. Use the $1 rule to question non-essential purchases.

Understand your net worth and track it.

Spend intentionally. Align spending with values.

Heal your money wounds. Address emotional triggers that lead to overspending.

Net worth trackers organize your accounts into cash & cash equivalents, investments, property, credit cards, and loans. Trackers mentioned in this book include Empower (free) and Monarch Money (paid subscription).

Budget:

Survive – basic necessities, including housing, utilities, food, transportation, and health

Revive – current expenses that aren’t necessary but make life worth living for you, such as vacations, clothing, entertainment, and hobbies

Strive – anything that helps you grow your net worth

The CRUSH method consists of 50% strive, 25% survive, and 25% strive. In other words, saving/investing half of your income – which does not seem attainable for most people, especially people who don’t earn six figures.The author mentioned that if this is not attainable, people should work to increase their income.

Other tips:

Remember that the interest you pay on any debt is making someone else rich by being their passive income stream. Ex: your mortgage, auto loans, and credit cards.

Unsubscribe from email marketing and digitally detox from constant comparisons. Reduce impulse spending.

Implement a $1 cost per use rule – technology, furniture, clothing, accessories, home goods.

Invest in a Roth IRA, where you won’t pay taxes on growth. All income earned is tax-free.

Compare insurance plan rates each year. Ask for discounts from service providers.

4 out of 5 stars

I look forward to reading, learning, and sharing more with you soon!

My intention is to post a Thoughtful Thursday column each week and share some of the insights I have learned in the past week. Here are some of the things I’ve learned this week:

Optimal Living Daily – How to Find Meaning in Life: 7 Steps to a More Fulfilling Existence

Define what it is that you want in life. What are your goals and aspirations? What brings you happiness and fulfillment? Be clear about what you want.

Connect with others and build meaningful relationships. When you have close relationships with other people, they can provide a sense of connection and purpose. Get involved in activities that bring you together with other people, such as clubs, groups, or social events.

Find your passion and do what you love every day.What are you interested in and what do you love doing? When you’re passionate about something, it brings a sense of joy and excitement into your life. You’ll be more motivated to pursue these interests, and you’ll feel more fulfilled when you’re doing them. Explore different activities and interests and see which ones make you feel the most alive.

Serve others and make a difference in the world. Helping others can give your life purpose and meaning. You’ll feel more connected to something larger than yourself, and you’ll have a sense of satisfaction from knowing that you’re making a positive impact in the world.

Live in the present moment and appreciate the here and now. When you’re constantly living in the past or future, you miss out on all the beauty that exists in the present.

Be accepting of change and understand that things will not always go according to plan. When you’re constantly expecting things to stay the same, it can lead to disappointment and frustration. When you accept change and understand that it’s a normal part of life, you’ll be more prepared for when things don’t go as expected.

Be your most authentic self. When you’re being genuine and true to yourself, it helps you connect more with others and build meaningful relationships. It allows you to live a more fulfilling life since you’re not pretending to be someone that you’re not.

The Jordan Harbinger Show – Sovereign Citizens – Skeptical Sunday

Sovereign citizens are people who don’t acknowledge the legitimacy of the United States government – don’t pay taxes, don’t have IDs, don’t register their cars, or acknowledge zip codes

They don’t believe the police or the courts have jurisdiction over them. They are not subject to the laws of the United States of America.

They represent themselves in legal matters and use pseudo legalese.

The roots of the movement grew out of White Nationalism. The modern sovereign citizen movement has an African American branch, the Moorish Sovereign Citizens.

Some sovereign citizens believe there are two classes of citizens within the United States: sovereign (original) citizens and federal (U.S.) citizens. Sovereign citizens have all of the rights of the Constitution but federal citizens don’t. Federal citizens voluntarily surrendered their freedom in exchange for benefits from the U.S. Government. Sovereign citizens renounce federal citizenship and reclaim the rights as common law citizens.

Sovereign citizen arguments have no basis in law and have never been successful in court.

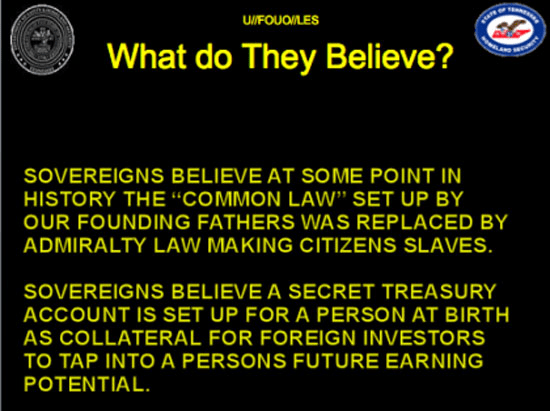

Sovereign citizens believe that you are not the person on your birth certificate. The birth certificate is its own entity. A birth certificate is ALL CAPS, a separate entity. They insist that the corporation that is the U.S. Government uses citizens as collateral to the Federal Reserve.

Sovereign citizens believe that as long as they don’t travel for commerce or cross state lines, they don’t need a license or registration. They will paint private use on their vehicles and issue themselves license plates.

Gurus sell sovereign citizen ideology. They appeal to desperate people, such as people in foreclosure or debt.

Gurus sell diplomatic immunity cards. If they create their own country and issue themselves cards that say diplomatic immunity, they believe they will have diplomatic immunity. Gurus also sell how-to books and membership cards. They are really just selling hope.

They believe that not only are you out of debt because your birth certificate is the one who owes the debt, not you, but that there is a bunch of money waiting for you somewhere. The corporations masquerading as our country owe you money.

Straw man account is the bank account attached to the corporate entity on your birth certificate (ALL CAPS) and this bank account is overflowing with cash – known as redemption. According to the sovereigns, the government set up secret bank accounts in our birth certificate names. They believe that with the magic words and forms, you can access it.

In 2016, the IRS discovered a sovereign citizen straw man scheme but only after issuing more than $43 million to sneaky sovereigns.

Bond process – by submitting the right set of papers, sovereign citizens believe they can wipe out their mortgage, tax bills, and student loans. Many people find themselves in the sovereign citizen movement through financial desperation.

There are between 200,000-300,000 people who consider themselves sovereign citizens.

The courts often reject sovereign citizen arguments without much explanation. No sovereign citizen has ever successfully argued their points in a court of law.

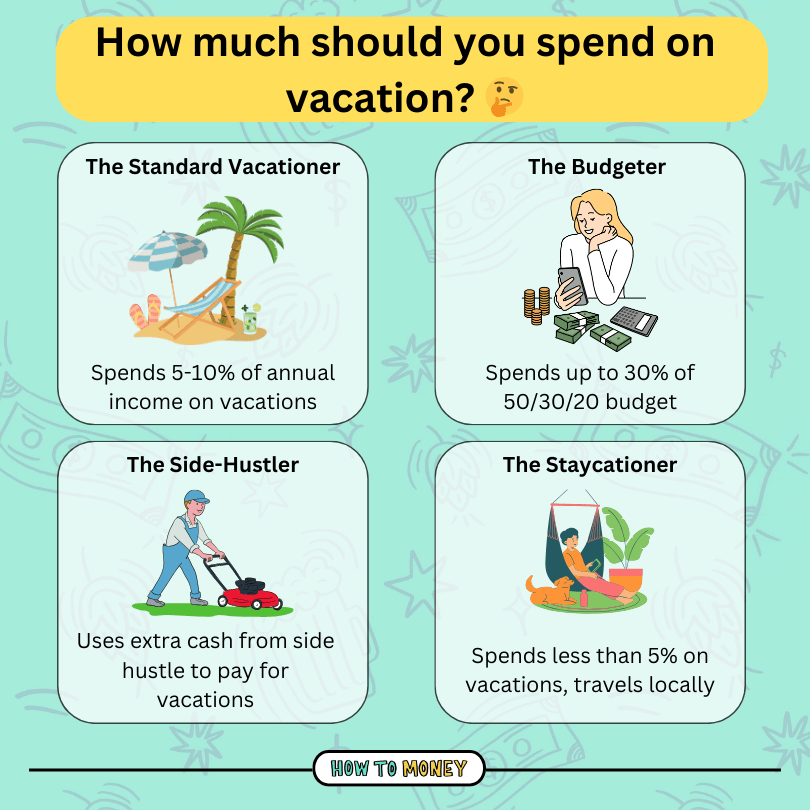

The Personal Finance Podcast – How Much Should You Spend on a Family Vacation?

This episode really surprised me. It suggested that people should aim to spend 5-10% of their net income on vacations (without going into debt). I definitely spend much less than that and instead have prioritized saving for retirement and short-term needs. I am curious to hear your thoughts about this!

You should never go into debt for a vacation.

Know your NET monthly income and monthly expenses. Know how much debt you have.

Have your emergency fund fully funded. 3-6 months of expenses

Be on track to hit your retirement goals. Investing your dollars is the only way to prepare for retirement.

Look at your short-term goals. Prioritize those goals.

Calculate your disposable income. Determine if there are any savings earmarked for vacation. Put savings in a high-yield savings account.

Automate savings using discretionary income – example: 5-10%

Once you build wealth, you may be able to spend 20-30% of your income on vacations.

By income:

$40k: 5% of net income – $2k per year on vacations/ 10%: $4k per year on vacations (will need to travel hack)

$60k net: 5%: $3k per year on vacations/ 10%: $6k per year on vacations (travel hack or side hustle)

$80k net: 5%: $4k per year/ 10%: $8k per year on vacations

$100k net: 5%: $5k per year/ 10%: $10k per year on vacations

Look for ways to increase your salary, get a side hustle, or learn to travel hack.

This post from Gabe the Bass Player stood out to me this week:

“If you are looking for chances to connect you will find them all over the place.

You’ll probably have to go first. It might be a little weird. It will be scary. You might not get the response you’re hoping for. You might over share. You might ask the wrong question. Your effort might not get reciprocated.

But it beats the alternative…

If you’re not looking for chances to connect, the depth of your relationships and your relational maturity are at the mercy of others’ initiative…and your indifference.“

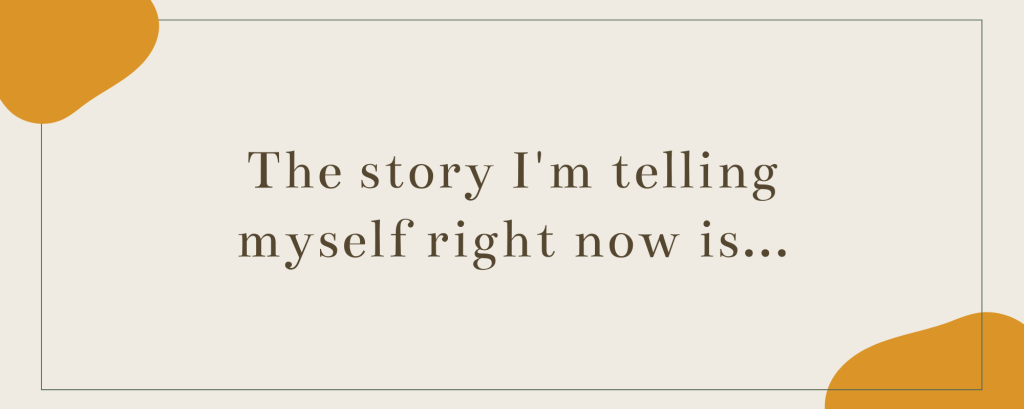

“What a simple verb. A five-letter modifier that opens the door to discussion.

If we state something as a fact, we’re asking for an argument.

But seems opens the door to learning and discussion.

What are you seeing that I’m not seeing?”

Often times we fail to see or consider other perspectives. We state something as fact, argue with others, and put the blame on others. We tell ourselves stories and accept them as truth. We forget that our feelings and thoughts are not facts. One phrase I’ve learned in therapy is “The story I tell myself is…” This phrase has been really helpful. Rather than put blame on others, verbally attack others, or believe my thoughts are truth, I put my thoughts out there with that phrase – and I have noticed that sometimes my perspective was wrong. I assumed incorrect intentions, didn’t have all of the context, etc. What story are you telling yourself?

I look forward to reading, learning, and sharing more with you soon!

My intention is to post a Thoughtful Thursday column each week and share some of the insights I have learned in the past week. Here are some of the things I’ve learned this week:

Optimal Living Daily – 8 Signs You’re A Perfectionist

You have the all or nothing mindset. The outcome has to either be perfect or there will be no outcome at all. You are either a success or a failure.

You fear failure. You have a fear of putting yourself out there and going out of your comfort because you might not be seen as “perfect.”

You might have trust issues. This has to do with the fear of letting go of control. You have the idea that if something needs to be done perfectly, you need to do it yourself. Letting go of this need for control and learning to trust other people is crucial for overcoming perfectionism.

You “should” all over yourself. You spend a lot of time in the “shoulda, woulda, coulda” land.

You procrastinate without end to find the right time to work on your goals.

You would rather give up than not do something perfectly. Putting decent work out there is a must to drive you all the way to your dream destination.

You spot mistakes everywhere. You see mistakes where other people don’t and you make it your mission in life to uncover them in all situations.

You fear judgment.The truth is that people don’t really think about you as much as you think they do. You don’t need other people’s approval to live your life; you just need your own.

Sad to Savage – Making Health and Fitness A Lifestyle With Savannah Wright

Make a plan for the week. Know that some weeks will be busier with events and obligations and you might not be able to work out as much as you want to. That is fine. Overall consistency is key, but not every week will be perfect.

Know that your body will change. You will need to alter your workouts. Don’t compare your body to how it was years ago. Your body may be looking for a different kind of workout.

Mindful mile – run a mile without music – focus on mindfulness – your breath and your thoughts

Yet, at the same time, you show up every day for work and for others. Show up every day for yourself. Don’t rely on motivation. Rely on self-respect, commitment, and dedication.

Give a new fitness program 90 days before deciding if it’s for you long-term.

Don’t wait until you “have the time.” Find the time. Prioritize yourself and your health.

If you can stream shows for an hour or hours, you have time to work out. You can even walk on the treadmill or lift weights while you watch.

Determine your why. Is it longevity? Physique? An event? You want to feel better? You’re only doing it because someone told you to do it?

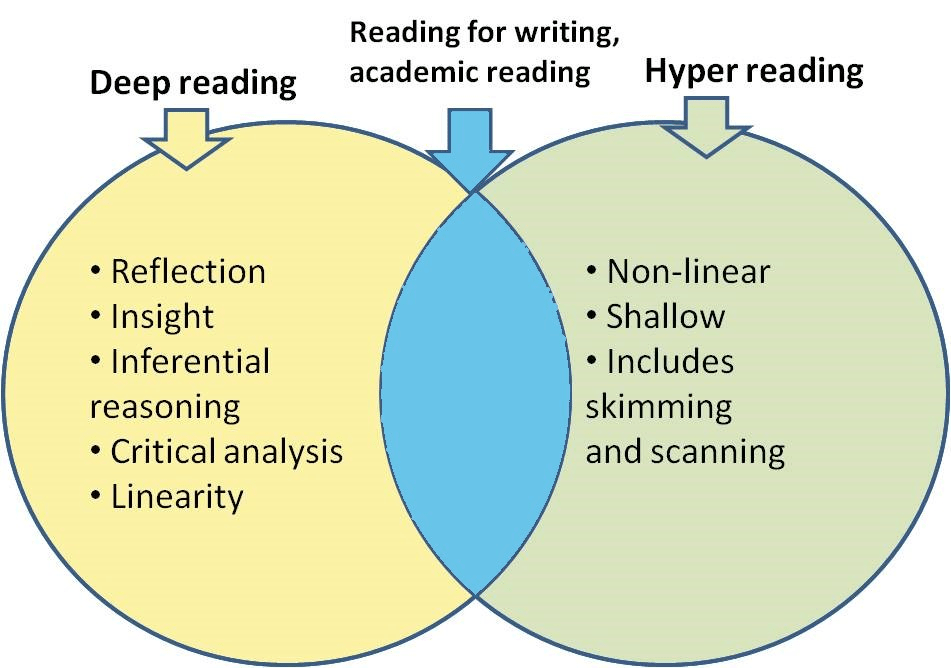

Life Kit – How to practice ‘deep reading’

Reading can be extremely difficult because things are competing for your attention. Our brains aren’t meant to deep read; it is supposed to be hard.

Reduce distractions.

Deep reading takes place when we become so immersed in deep thought and concentration and don’t give in to distractions.

We tend to skim instead of deep read. Skimming is one of the greatest disruptions of deep reading. It’s a defense mechanism.

Screens are fine if you are skimming. If you want to deep read, you have a better chance of minimizing distractions if you read on paper, where you can go at your own pace.

Start by forcing yourself to read at least 20 minutes per day in print – not on screens.

Deep reading takes practice, discipline, and finding time devoted to it each day.

Do not be concerned about how many books you are reading. People read at different speeds and different books require different paces. Let the book determine your pace and enjoy your own pace.

There is more memory that consolidates than we have immediate perceptible access to. On the other hand, when we skim, we consolidate less. Taking notes adds to your ability to remember and reading the notes about what you read activates what you actually did remember and have stored.

Deep reading is a place of discovery of others, discovery of beauty, and discovery of appreciation for our ability to think outside the bounds of our everyday lives.

Real Simple Tips – 5 Grocery Items to Avoid, According to Professional Chefs

Store-bought pesto – hard no for many. It is so easy to make at home with whatever greens you like and need to use up, and you can make it dairy-free if needed.

Jarred tomato sauce – full of sugars and preservatives. Instead, buy canned, whole, organic tomatoes, blend them up, and cook them down with your favorite aromatics in twenty minutes.

Premade salad dressings – make your own with olive oils, lemon juice, garlic, and herbs.

Boxed broth – save your veggie scraps (carrot peels, herb stems, garlic skins, etc.) and make broth when you have enough scraps. Use your veggie scraps with water, salt, and herbs and refrigerate or freeze batches.

Pre-grated parmesan – seek out parmesan and grate it fresh when you need it.

This list surprised me. I love cooking, although I am not a professional chef. Still, to save time, I buy jarred tomato sauce, premade salad dressings, and boxed broth!

The Personal Finance Podcast – Why Most Americans Are Poor (And How to Change That)

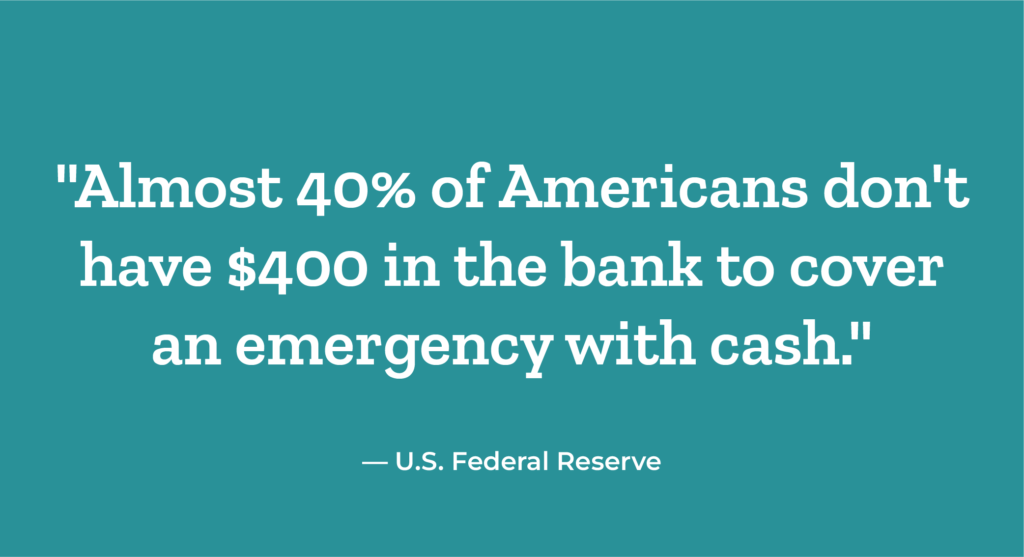

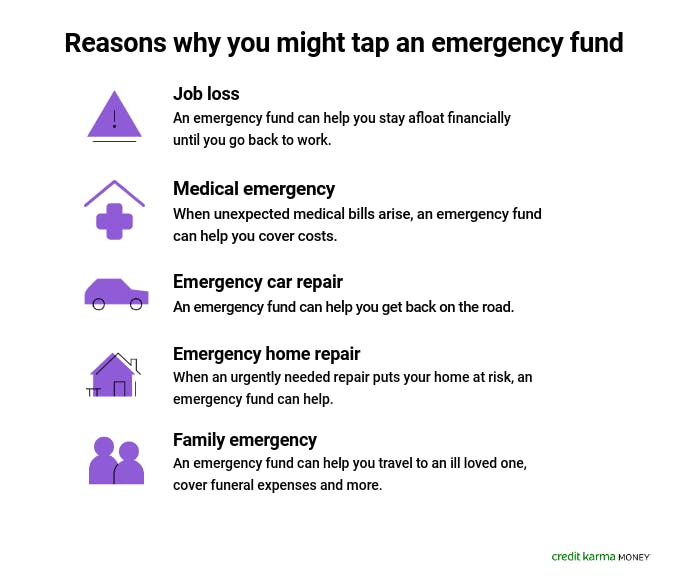

Credit card dependence – don’t use credit cards as an emergency expense vehicle. Have an emergency fund in place and take the time to build it up. Nearly half of Americans use credit cards to cover essential living expenses. Nearly half of Americans have reached their credit card limits at some point.

If you aren’t making enough money to make ends meet, reduce expenses or increase your income. When you fall into credit card debt, you are paying an extremely high interest rate (often over 20%). Compound interest can cost you thousands of dollars. If you struggle with credit card debt, get rid of your credit cards and force yourself to make it work. Your credit card debt is robbing you of your financial freedom.

Decreased financial preparedness – when you are trying to build up your emergency fund, it can seem like you will never get ahead due to emergencies. You are likely either spending too much money or not making enough money. Income is the propeller that allows you to build more wealth. Have an emergency fund to protect you from life – medical deductible, vet, car repairs, etc.

Focus on how to get extra cash on hand. Open a high-yield savings account and automate contributions. Put at least $5,000 in a high-yield savings account then start to work up to 6 months of your monthly expenses.

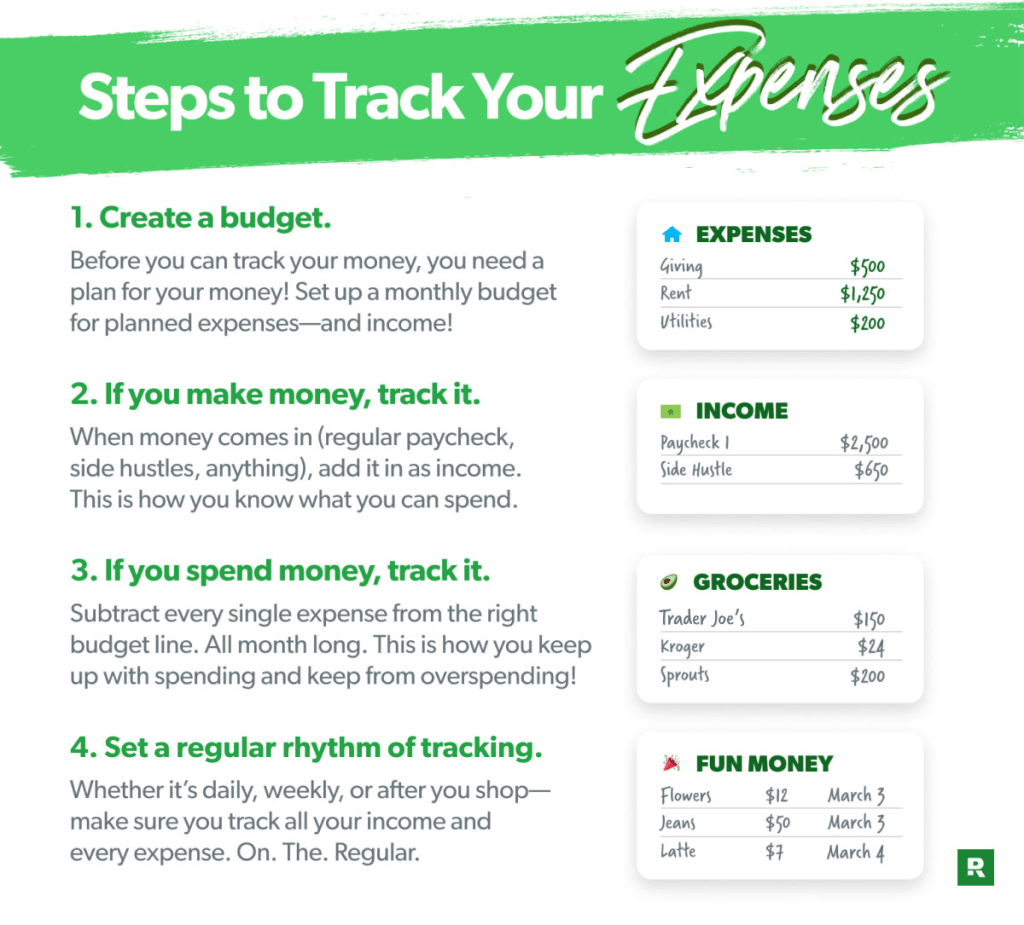

People do not prioritize money flow. Figure out how much money you have coming in and where that money is going to go. Keep a list of all of your income and expenses in a spreadsheet.

First, focus on housing, food, and transportation and get those expenses down. Car payments, groceries, and eating out are easy expenses to overspend on. Get them under control.

People worry about $10 problems instead of bigger problems: investment fees, mortgage interest, asset allocation, negotiating your salary, transportation costs, and student loan interest. Some of these will cost you six figures over time!

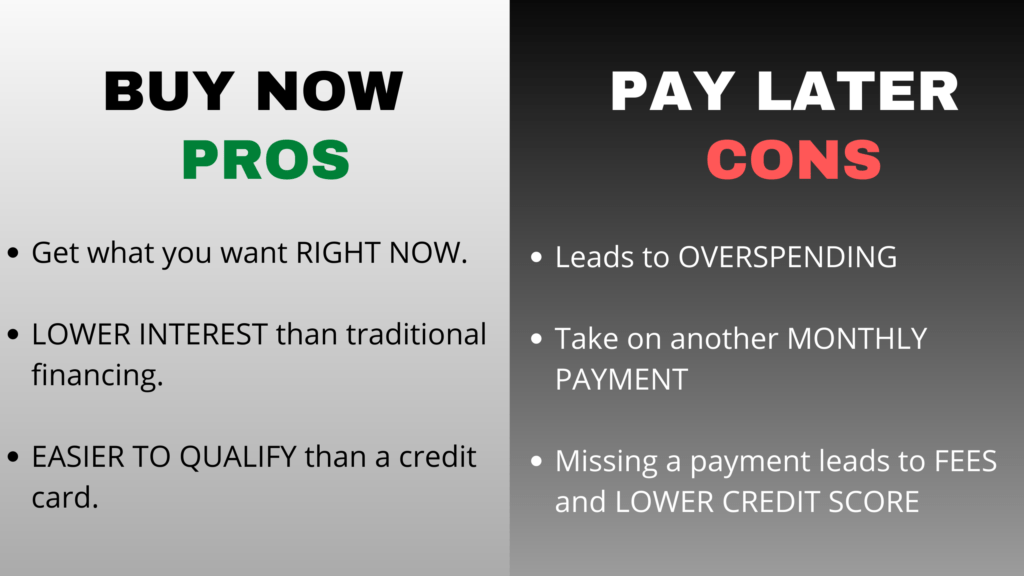

Over-reliance on buy now, pay later services for basic necessities – many people do it to avoid credit card interest. 46% of people use buy now, pay later for electronics, 56% use it for clothing, and 31% use it for furniture and appliances. Instead, save up for these items. If you don’t have the money, don’t buy it. Focus on building up your emergency fund. Buy now, pay later increases your debt volume, reduces your net worth, and can result in late fees and financial penalties

Lifestyle inflation and mismanagement of raises or bonuses – when you get married, it is easy to increase your lifestyle and want to do more. However, it’s still important to have a gap between your income and expenses.

Every time you get a raise, put half of it toward investments and allow yourself to use half of it to increase your lifestyle.

Lack of financial education and planning – can use a financial planner (can cost a couple thousand dollars), take a class, or read books and research yourself

Low national savings rate – the average American saves 3.6% of their income. You need to save and invest the savings to retire. Experts say to save at least 20% of your income (and invest it) so that you can be able to retire. Some people save 50% of their income to retire very early!

People are trying to access their retirement funds early and doing it often – 10% penalty. Don’t do that. Don’t interrupt compound interest unnecessarily. This year, Americans will pay $6.1 billion in penalties for early 401k withdrawals!

People don’t understand compound interest – they don’t realize how much it impacts your finances and retirement.

I look forward to reading, learning, and sharing more with you soon!

My intention is to post a Thoughtful Thursday column each week and share some of the insights I have learned in the past week. Here are some of the things I’ve learned this week:

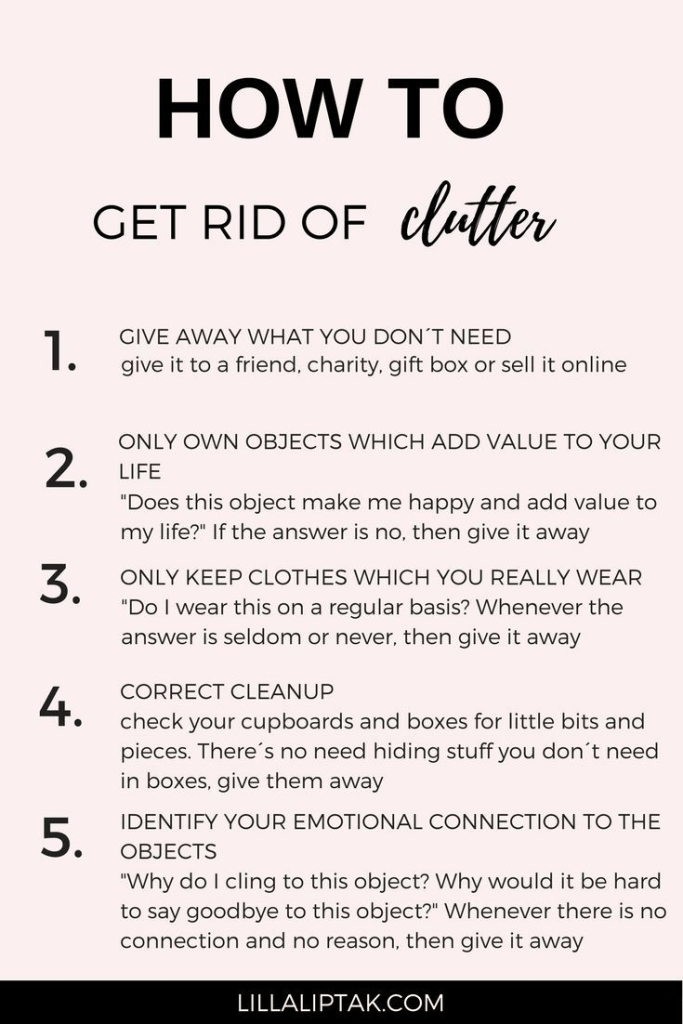

Frugal Friends Podcast – Declutter Your Home in 30 Days

Grab a box, walk around your home room by room, and put anything you don’t need in the box. Start with the easy stuff. Do this several times.

Find motivation with built-in deadlines. Set a timer for 15 minutes and do the first wave in 15 minutes.

Donate more. Use your local Buy Nothing group or Facebook marketplace. You can try selling what you would like to. If it’s not sold within a week, donate it.

Have people in your household help you declutter. Have them find things they would like to give away or donate.

Don’t rent a storage unit long-term. If you want to rent a storage unit short-term, pack up boxes and label them with a date. If, after 6 months to 1 year, you don’t go to your storage unit looking for that item, get rid of everything in the boxes, and get rid of the storage unit.

Plan to have people over to give you a sense of urgency to get rid of the clutter. Use that as a deadline for you to declutter.

Don’t confuse the desire to change with actual change. Thinking about change is not the same as implementing change.

Spending money on something does not result in that hobby or activity getting done.

Challenges

10 minutes, 10 spaces – 100 items. Get rid of 10 items from each of 10 different spaces, for a total of 100 items.

Minimalist challenge – get rid of 1 item on the 1st of the month, 2 items on the 2nd day, and so on, so on the 31st day of the month, you will get rid of 31 items. This challenge is often unfinished. You can do this challenge backwards – start with getting rid of 31 items, then 30, etc.

Ask yourself: How do I actually foresee myself using this in the future? How much would it cost if I got rid of this and then suddenly needed to get it again? Where am I going to keep this item?

If you haven’t used it in the last year and it costs less than $20 to replace it, get rid of it.

Last January, I got rid of one thing each day in our local Buy Nothing group. This year, so far, we have started decluttering one spare room that has been filled with boxes we haven’t really touched since we combined our belongings over a year ago. We have organized what we are keeping, we have thrown a lot of junk away, and we have made piles to give away. It is crazy to think about how much stuff we don’t actually need/want!We have several more spaces/rooms to declutter yet, but it is exciting that we started.

Life Kit – The decluttering philosophy that can help you keep your home organized

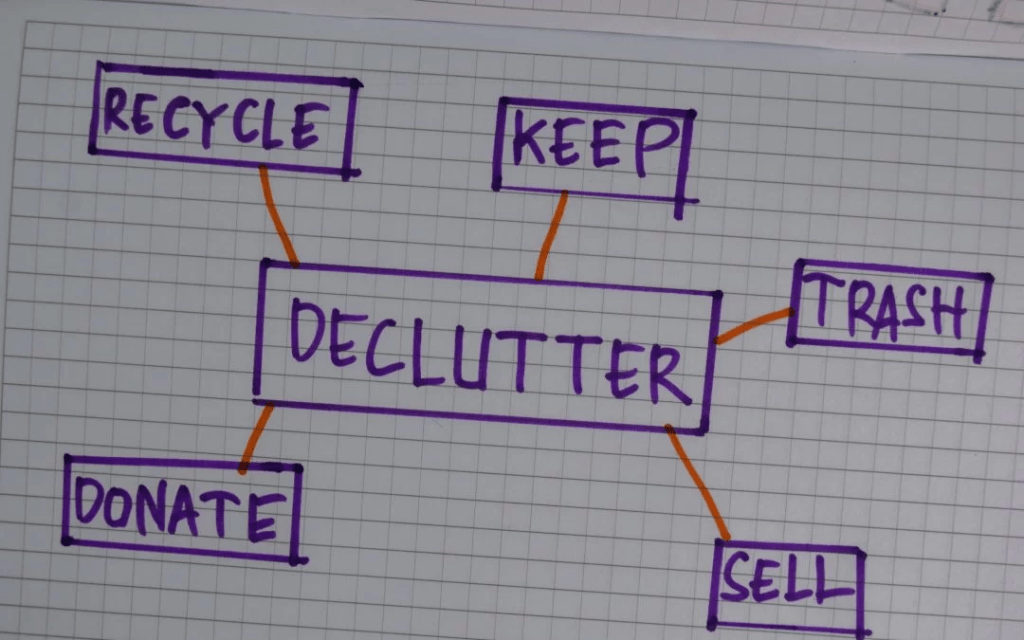

Start in the easiest place first – not paperwork or sentimental things. Decide what should stay or go. If you decide to get rid of things, get it out of the room/space right then to eliminate clutter.

After you decide to keep things, find a space for them.

The smaller the space, the more intentional you need to be. Ask yourself: What are the 3-5 activities you want to do in this space? How do you want it to look? How do you want to feel?

Fit, Healthy & Happy Podcast – 10 Life Changing Things I Learned in 10 Years of Lifting

You will never be at an “end point.” You will crush goals and create new goals. Learn to love the process and appreciate how far you’ve come.

Training to failure is overrated. Do a specified number of reps and don’t overtrain.

Nothing beats consistency. Set realistic goals.

Lifestyle adaptation – fight laziness and enjoy the process.

You’re not giving 100%. You’re typically capable of a lot more than you think.

Supplements are way less important than you think. Supplements are supplemental to a great diet, great training, and a great mindset.

If you find something especially hard, do more of it. Ex: cooking, hard exercises, fixing sleep schedule. Fix your weakness.

Keep learning and reading. Question everything and try to have a deeper understanding of it.

You should be doing this to be healthy, not just look sexy.

Form will always be one of the most important things. Without the right form, you’re either getting injured or you aren’t getting the most out of the movement.

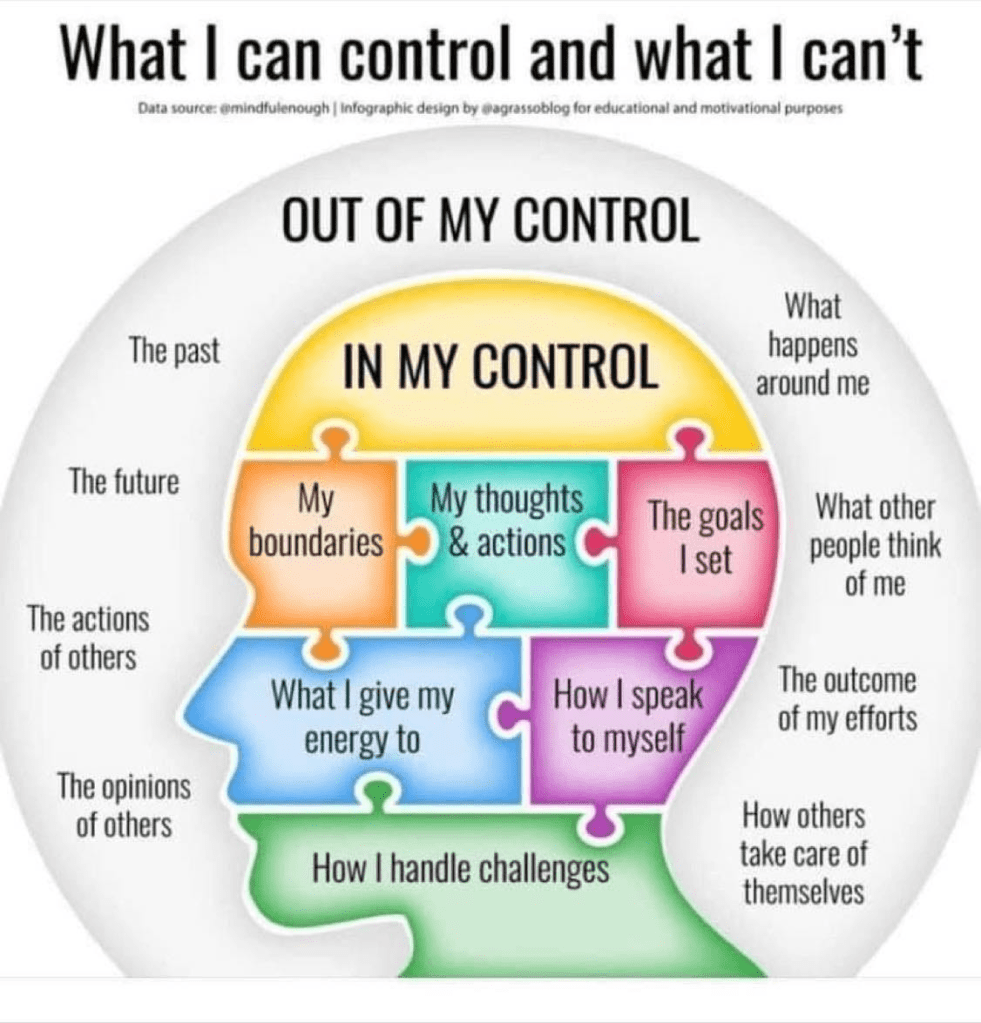

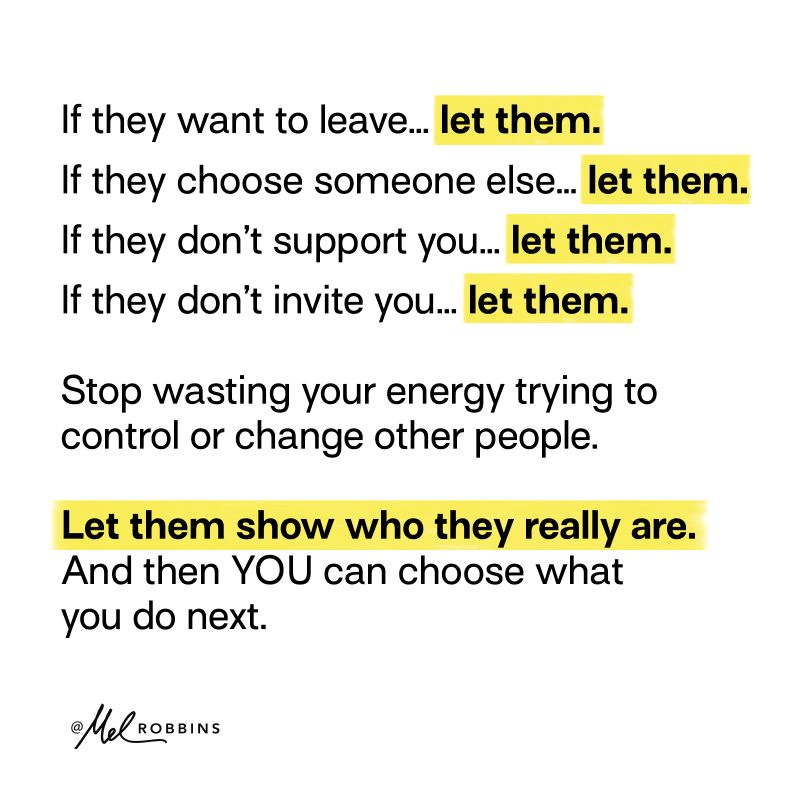

Whenever someone is doing something you don’t like, let them.

You will be more in control when you use the “let them” theory. You stop giving your time and energy to other people and situations you can’t control. You take your time and energy back and figure out what is best for you.

The more you try to control something, the more out of control you feel. The only way to feel in control in life is to focus on where your time and energy is going.

Everyone has an opinion of you. Unhook yourself from that concern. Their opinion of you is irrelevant to you.

It’s not your job to manage other people’s reactions. When you think about how often you are managing other people’s reactions, managing other people’s happiness, tiptoeing around the topics, shrinking yourself, staying silent, not asking for what you need, trying to fix problems, showing up when you don’t feel like it, doing things out of guilt, you are resisting the reality of the situation. When you think about it, you will realize how much time and energy you have and how much time and energy you can spend on yourself.

You aren’t responsible for other people’s happiness, other people’s boundaries, or managing other people’s tantrums. You’re responsible for your truth, your needs, expressing yourself, and telling people how you feel. You’re responsible for creating what you want.

When we step in and feel the responsibility for bailing people out, we rob them of the opportunity to face the things they didn’t face.

You can’t force anyone else to change or to do something. You can try, but someone only does something because they want to do something.

Optimal Finance Daily – 6 Things You Should Never Scratch Off Your Budget

Savings – emergency fund + retirement – even if you don’t have much money to save now, starting will help ensure that you’ll be better off financially down the line. At a minimum, contribute enough money to get an employer match.

Health insurance – make sure you have insurance in case you experience a major illness.

Debt repayment – have a plan to pay down student loans, credit cards, and other high-interest debts as quickly as possible. Consider getting a side hustle or working overtime to increase your income and pay off debts.

Life insurance – make sure your dependents are covered if something were to happen to you tomorrow. Adjust your life insurance policy as needed; you may need to take out more money as major expenses occur or as you have more children.

Spending money – put aside some money to spend – don’t spend it all at once. Sometimes having something now isn’t worth incurring interest charges down the road.

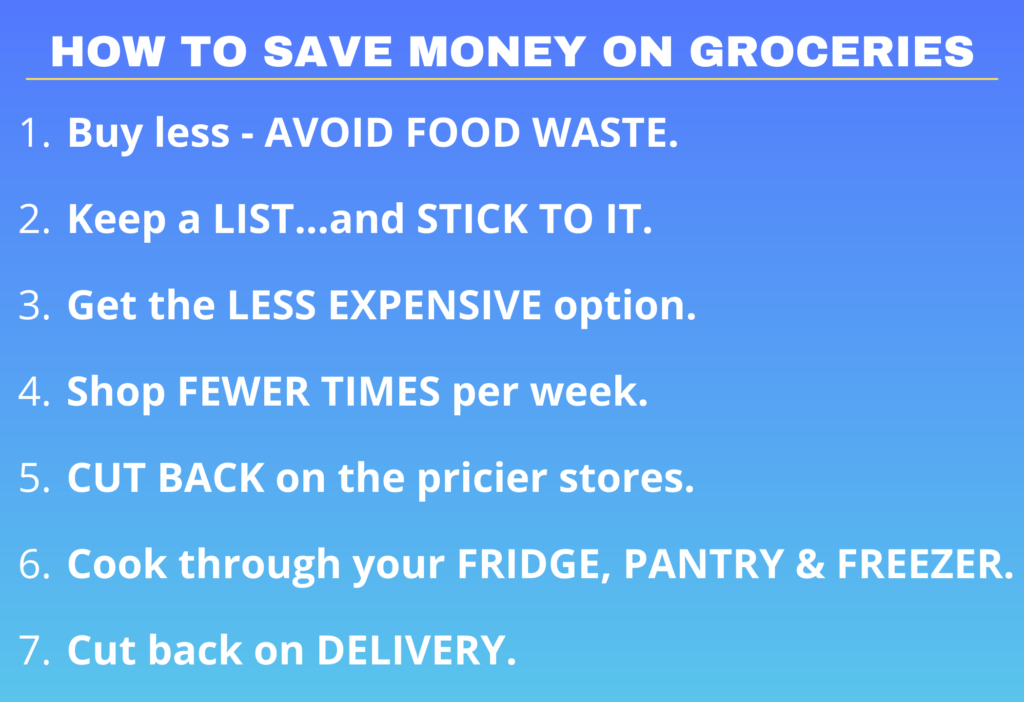

Groceries – know what you can afford on a weekly basis. Look into ways to cut back without dramatically impacting meals, such as shopping at discount stores or taking advantage of coupons and sales. Remember that eating out often will quickly eat away any extra money you may have had available in your budget.

To save money, we shop at a discount food store, keep some staples on hand, and we frequently plan meals around what we can find at a discount rather than planning around recipes or a list.

Optimal Finance Daily – Stop Using These 6 Ridiculous Excuses For Not Saving Money

The first step to saving more money is to figure out why you are unable to save money.

“I’ll hate my life if I start saving money” ➡️You can still live a great life AND save money. You need to learn how to manage your money better so that you can live the life you want to live, but on a more realistic budget.

“I’ll figure out how to save money later.” ➡️Many people put off saving because they’d rather spend their money now and believe they’ll have plenty of money to save money later. There is no need to spend all of your money now just because you can.

“I deserve and/or need the things I buy.” ➡️Many people believe they need to upgrade to the latest and best technology, clothing, etc. and need expensive vacations. Watch your spending, figure out ways to lower your expenses, and cut out anything unnecessary.

“I enjoy my job and can always make money.” ➡️You should still be saving money. What happens when you can no longer work? You don’t know what the future will bring – a medical problem, a serious life event, or you may hate your job later. You can enjoy your job and save money at the same time.

“The city I live in is too expensive to save money.” ➡️It may take time, but you need to either increase your income or cut your expenses or do both.

“It’s too late for me to start saving money.” ➡️It’s never too late to start saving money. Every little bit helps and can drastically change your future. Saving something is better than nothing.

I look forward to reading, learning, and sharing more with you soon!

My intention is to post a Thoughtful Thursday column each week and share some of the insights I have learned in the past week. Here are some of the things I’ve learned this week:

Self Improvement Daily- Earn Respect, Not Validation

Our interest to prioritize and maintain strong social connections is fundamental to our success as a species, and in order to appease our ego, we seek validation, approval, and acknowledgement from others as a means to confirm our importance. This may cause us to do things that aren’t in alignment with who we want to be because we need quick access to the validating spike of feeling important.

What we’re actually searching for, that leaves a deeper and lasting impression, is other people’s respect. This goes beyond what you do and into who you are– your character and your values. This is more difficult to earn, and in a society that is addicted to immediate gratification, sometimes people don’t even have the patience to get there.

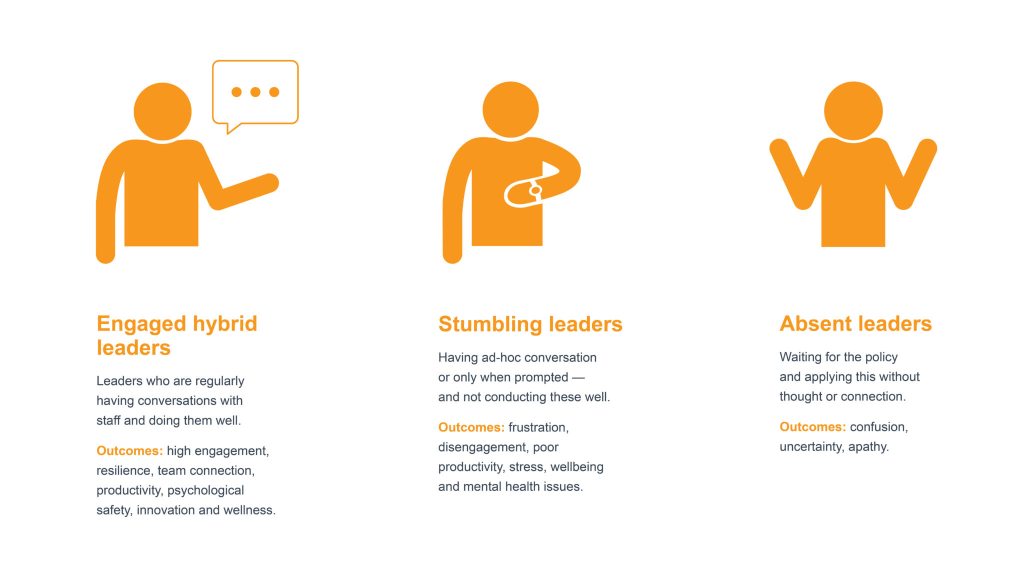

Ted Talks Daily- 4 ways to make hybrid work better for everyone

I was surprised to learn that, using surveys, polls, and meta-analyses, over 70% of employees in most global surveys want a mix of in-person and remote formats moving forward.

Many employers unexpectedly moved to a remote or hybrid format during the COVID-19 pandemic. Many also haven’t put much thought into a plan. Some employers want employees in the office a certain number of days each week, but don’t care when. Others haven’t set expectations. Others have clear expectations about when employees need to be in the office. Here are 4 ways to make hybrid work better for everyone:

Coordinate anchor days — days you and those you collaborate with are in the office on the same day.

Plan spontaneity. Set aside 6-7 minutes of online meetings to chat informally about something other than work. Consider happy hours, trivia challenges, or lunches or coffee with coworkers.

Match digital tools with communication objectives. Sometimes e-mails, IMs, and phone calls won’t cut it. Use video calls for conversations when needed.

Consistency between hybrid policies and attitudes is the only way to build a hybrid culture for everyone. If you want your employees to come in a certain number of days, assign days or make that expectation clear. If there aren’t any clear expectations and people don’t come in the same number of days, nobody should be made to feel guilty for not coming in as often as others.

Optimal Finance Daily- Budgeting Tips: 10 Ways to Lower Your Life’s Fixed Costs by Joshua Becker

Buy or rent a smaller home. Housing costs generally take up the largest percentage of a person’s expenses.

Avoid car payments.

Double-check recurring expenses and cancel any you no longer need or use.

Research insurance costs. Double-check your premiums and compare other options.

Take your lunch to work.

Pay off your credit card debt. Interest payments are like flushing dollars down the drain. We don’t receive anything for them.

Stop upgrading your phone just because you are eligible.

Cut utility bills at home. Get a programmable thermostat, lower the temperature on your water heater, unplug unused electronics, cut cable, or seal your home better for cold and heat.

Research childcare options in your area. Sometimes new childcare centers are much less expensive than the one your child or children is currently enrolled in.

Ditch the storage unit. If your storage unit is simply storing stuff because you own too much stuff, get rid of it. Stop paying money to keep stuff you don’t need.

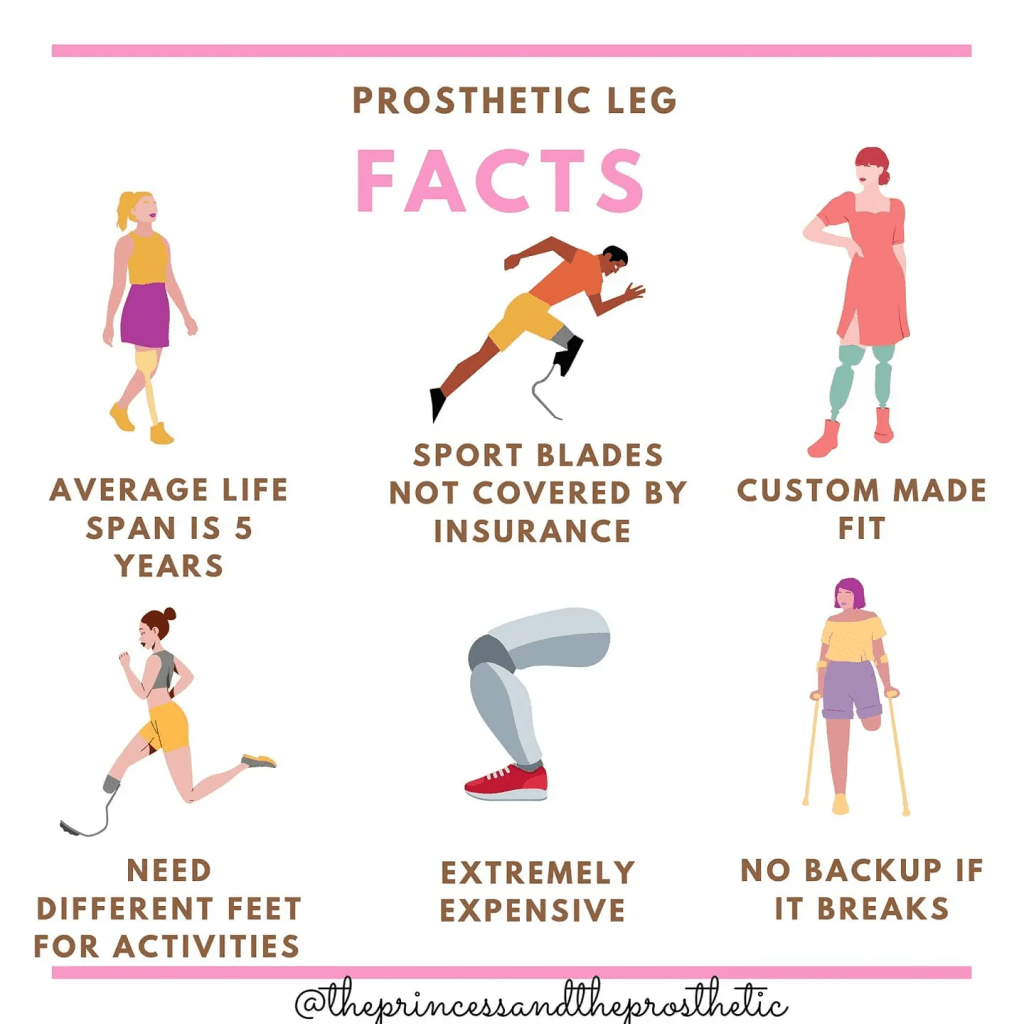

The word “prosthetic” is Greek. When translated to English, it means “addition.” A prosthetic is a device that provides support in place of the body part so that people can perform day-to-day functions.

In ancient Rome, there are accounts of warriors who used prosthetics made of iron and wood to make artificial arms and legs.

Thousands of years ago, prosthetics were cosmetic.

During the French Renaissance, prosthetics became functional and included harnesses and knee lock controls, as well as softer materials.

Limb loss can be caused by a disease or cancer that impacted that body part, a car accident, or being born without a body part.

Prosthetics are made according to what body part is missing. How it looks and how it is made is dependent on the person and body part. Generally, measurements are taken and a cast is made. A mold is made to specifications. It is shaped to be comfortable for the patient. Most prosthetics are constructed with lightweight carbon fiber, aluminum, and titanium components.

Nearly 75 percent of amputations are caused by diabetes and cardiovascular complication. The most common type of amputation is a below-knee amputation.

The average prosthetic lasts *only* three to five years!

Most amputees wear a stump shrinker, which is a compression sock that keeps the limb from swelling when the prosthesis is not on their limb. Most amputees wear a silicone gel liner that helps to cushion and protect the limb during walking.

Since ‘best’ isn’t defined, the guarantee is also meaningless.”

Gabe the Bass Player at gabethebassplayer.com

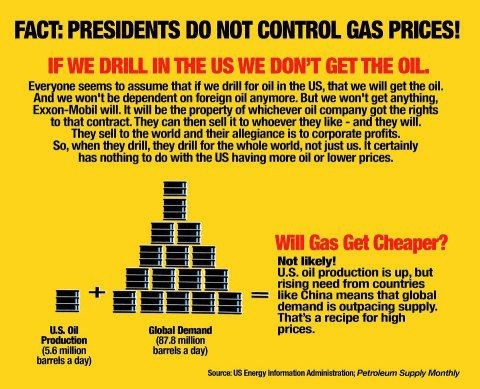

The Economics of Everyday Things- Gas Stations

In the U.S., Americans use 374 million gallons of gas every day!

Gas is cheap in the U.S. relative to other countries. Considering the amount we use, though, every penny counts.

We often blame politicians and oil executives, but the easiest target is the gas station owner. There are 145,000 gas stations in the U.S. 8 out of 10 are independently owned and operated. They pay oil companies for the right to use their branding and gas. Many come from other countries.

50-60% of cost of gas is from the cost of crude oil. $4.00 cost of one gallon of gas= $2 cost of crude, 70 cents to refine it, 40 cents to move it from refinery to gas station, 50 cents for federal/state/local taxes. For a $4.00 gallon of gas it costs about $3.60 to get it to the pump. Gas station owners make about 30-40 cents out of every gallon they sell, which has to cover maintenance, electric bill, rent, liability, etc. In the end, they are averaging 7 cents per gallon of profit.

Gas stations have a daily profit of about $300 after all expenses.

Gas stations regularly face competition with other area gas stations.

Station owners usually buy a few days of gas at a time and store it in underground tanks, but the price of wholesale gas changes every 24 hours. As a station owner, you can lower your prices and lose money or keep a little profit margin and watch your customers go to another station.

When crude prices go up, station owners are slow to pass on the extra cost to us at the pump, but when they fall, they don’t set the prices lower right away either. When gas prices increase, tight margin on gas gets squeezed even further, people buy less gas, and people also buy less inside the store. Higher gas prices also result in more theft.

Gas isn’t a big money maker. The bulk of a gas station owner’s income comes from selling food, where they have an average 33% gross profit inside the store.

Healthier Together- How to Know if You Should Have Kids + Debunking Myths About Parenthood

I don’t have kids (yet), so this was an interesting podcast with different perspectives and insights!

Many people ask “Are you going to have KIDS?” One point the podcast host made is “How will you know whether you want to have KIDS (plural)? Should I have KID? Then you can decide whether you should have KIDS.”

The most surprising point I learned on this podcast is that the ideal age to become a parent is said to be 38 or 39! This provides time to enjoy two adulthoods: 18-38 can be spent traveling, establishing your relationship with your partner, establishing your career, etc. Another adulthood starts when having kids at 38 or 39. This also results in having wisdom, perspective, and better finances, and, if you live long and are healthy, your kids can still care for you when you are old.

Many people have kids earlier due to societal or family pressure or the fear of infertility. If you have concerns about fertility with waiting, check with your doctor about fertility tests and risks. This makes more sense than having kids earlier simply due to this sometimes-unreasonable fear. Some fertility treatments are covered by insurance or are available through grants.

If you are concerned about finances, you can save money through hand-me-downs, secondhand retail, community or church groups, and neighborhood exchanges. You can also do a childcare exchange with friends.

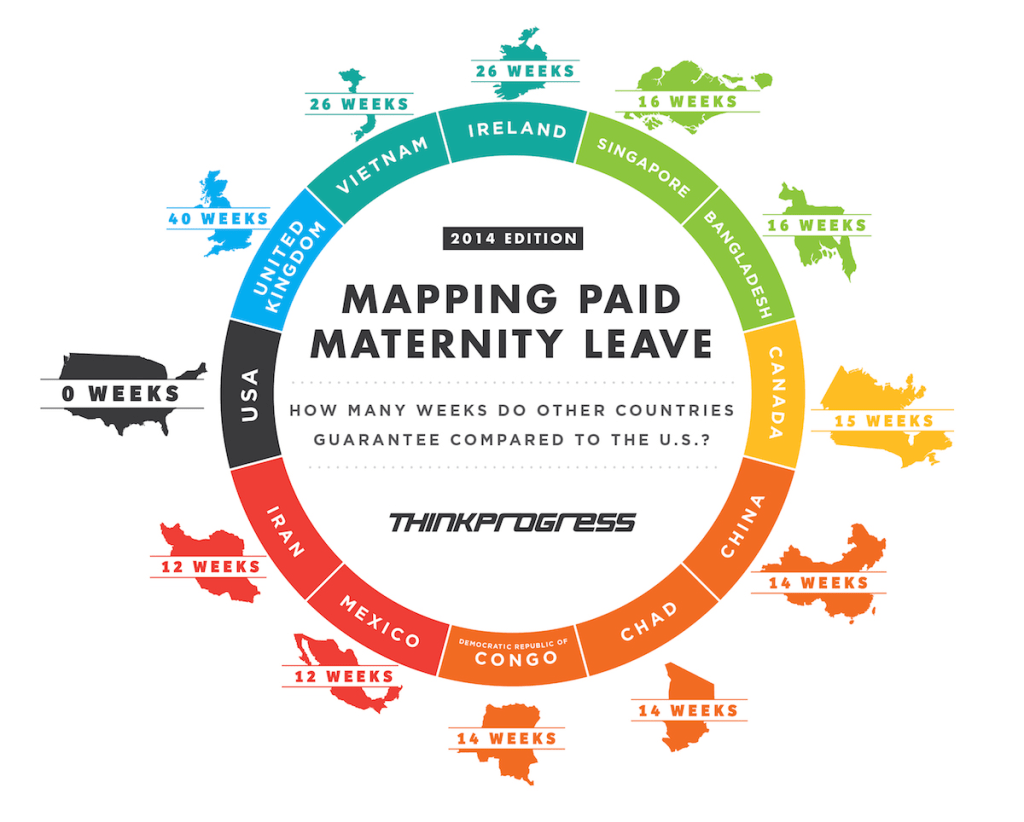

Our society says we value children, but we do not put the $ or attention there. Many employers do not offer paid maternity or paternity leave, resources, or flexibility for childcare, etc.

You may never feel 100% confident in your decision to have kids. That’s okay. 60/40 confident is enough. It isn’t about baby or no baby. If you are postponing or thinking about not having kids, ask yourself if there’s anything you haven’t done yet in life that needs to happen. We will have some disappointments. Ask yourself “What hasn’t happened yet that I want to happen between now and when I die?” It’s about thinking about what is important to you that hasn’t happened yet and how you will fit that in. Be able to name those things and think about, if you actually have extra time and $, are you really going to do those things?

If you are afraid to bring a child into this world, know that people were also worried in the 80s and other decades. There have always been big issues dominating our consciousness and people still chose to have children and have not regretted it. There is always going to be some concern or worldly issue.

There is a lot of stress involved in raising kids, but the major factor is whether the child was planned or an accident and whether the parents had a close, high-quality relationship before having a child. Once kids are grown, parents rave about being parents.

There are many ways of finding life satisfaction and meaning even without having kids. Many parents do say that having kids has brought the most happiness in their lives, but that does not mean that you need to have kids to be happy. Volunteering, hobbies, career fulfillment, being a coach, and many other things can also bring meaning and happiness.

You can get to know your partner better than ever before just by thinking and talking this topic through. It’s not just “yes” or “no.” What are your fears? What do you want your life to look like? How will you share in the responsibilities? What is important to you?

I look forward to reading, learning, and sharing more with you soon!