“101 Things I Learned in Culinary School” was written by Louis Eguaras with Matthew Frederick. Louis is a department chair at the Culinary Arts Institute at Los Angeles Mission College, Chef Instructor at the Institute of Culinary Education, and a former White House Chef. I read this book back in 2023. This book is not a recipe book! Instead, it contains practical how-tos and interesting facts. Here are some of the many facts that stood out to me.

Guests seek more from a dining experience than to satisfy their appetites: comfort, prestige, value, relaxation, artistry, social fun, or perhaps just a good place to watch the game. Be clear why customers choose your restaurant. Prioritize what they most need.

Keep guests informed. Be open about errors and oversights – understaffed, dish running late, etc. Acknowledge mistakes!

Repurpose rather than reuse. Have multiple uses for every food item. Repurpose preparation scraps and use in stocks, soups, purees, etc.

Liabilities for restaurants: food-related illnesses, chemical hazards, physical hazards, property hazards, drinking hazards/serving too many drinks

School teaches you how to cook. Experience teaches you how to be a chef. A cook follows a recipe; a chef can intuitively modify a recipe. A cook knows how; a chef knows why.

Kitchen lingo:

“all day” = the total # of items to be prepared. Ex: 2 burgers rare + 1 burger medium = “3 burgers all day“

“dragging” = not ready with the rest of the order. Ex: “The fries are dragging.”

“drop” = Start cooking. Ex: “Drop the fries.“

“fire” = Start cooking, but with more urgency. Ex: “Fire the burgers.“

“on the fly” = with extreme urgency. Ex: “Get me two soups on the fly.“

Mise in place is a practice and a philosophy. Determine everything you need before starting a dish or shift – recipes, ingredients, utensils, pots, pans, stocks, sauces, oils, dishware, and anything else. This permits the most efficient use of a cook’s space and time and informs the disposition and posture of a chef.

Shake hands with a knife. To hold a chef’s knife properly, rest your thumb on one side at the juncture of the blade and handle, and let your middle, ring, and pinkie fingers grip the handle naturally on the other side. The index finger rests on the side of the blade, near the handle.

4 ways to tenderize:

mechanical (pound with a mallet before cooking)

marinade in an acidic bath for 30 minutes to 2 hours

salting/brining – coat with coarse salt and refrigerate for 1-4 hours, then rinse off and pat dry before cooking

slow cooking in liquid in a slow cooker

Food keeps cooking after you stop cooking. Allow for carryover cooking in meats by removing them from the heat source when the internal temperature is about 5 degrees Fahrenheit below the safe-to-eat temp. Let sit for 5-10 minutes and monitor the temperature.

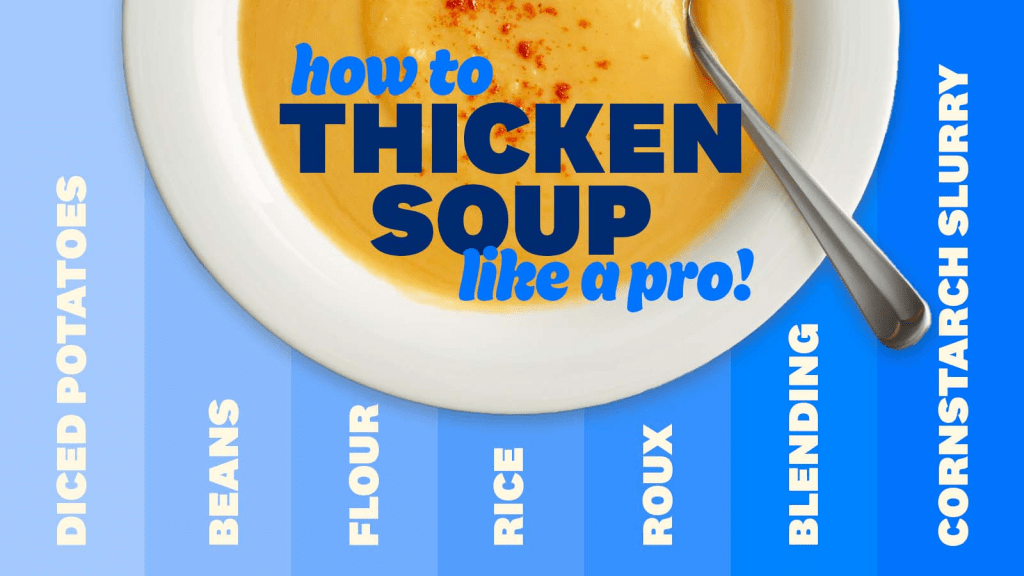

Ways to thicken a stock, soup, or sauce:

reduction (remove the pan lid and simmer until desired thickness is achieved)

roux (heat butter in a saucepan, and slowly add an equal amount of flour, stirring constantly to produce a paste)

slurry (cornstarch for dairy-based, arrowroot powder for acidic sauces)

gelatin

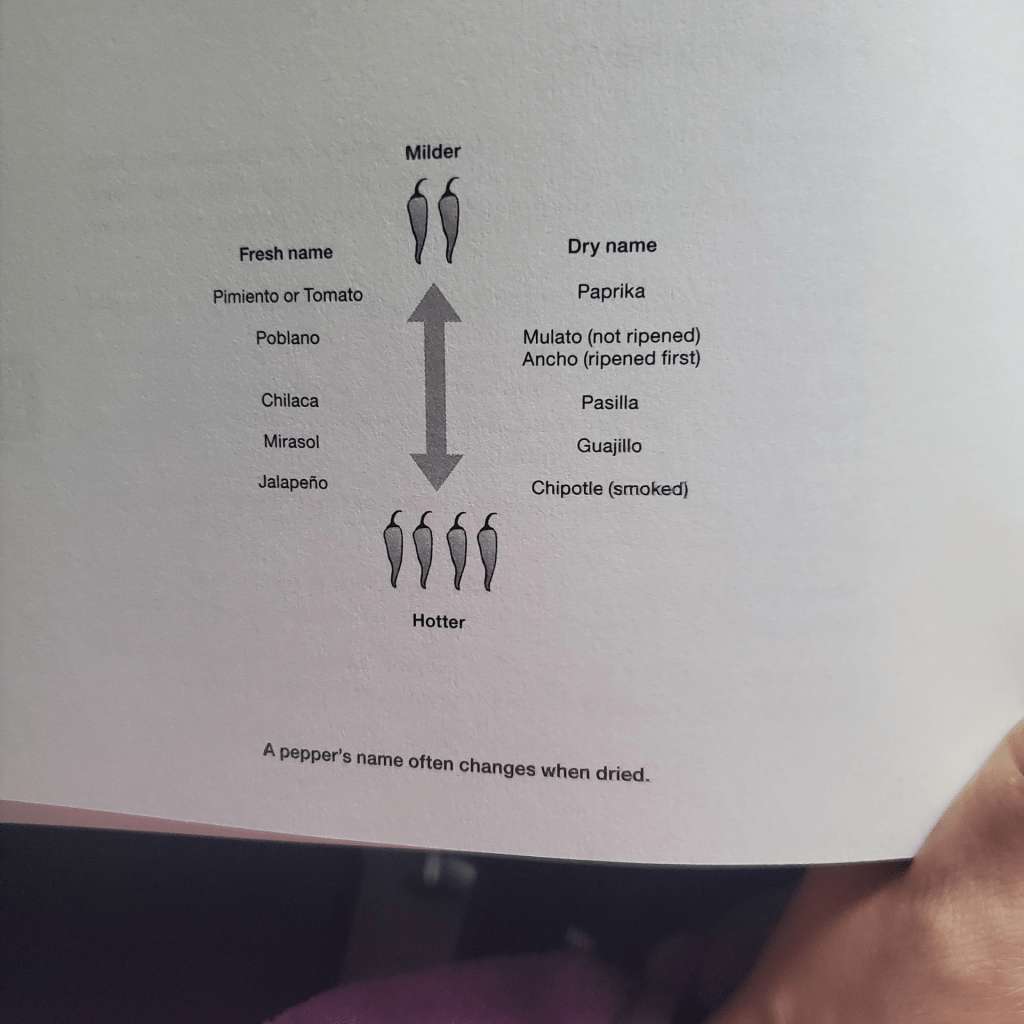

A pepper’s name often changes when dried.

Fresh pimiento ➡️paprika

poblano ➡️ mulato (not ripened) or ancho (ripened first)

jalapeno ➡️chipotle (smoked)

Menu types:

static (common chain/fast-food restaurants)

cycle (changes daily/repeats weekly)

market (based on what is available for purchase by the restaurant daily)

farm to table, a la carte, prix fixe, etc.

Serve a just-enough portion. The protein should be about the size of the palm of your hand, and the vegetables should span about 2 or 3 fingers. A just-enough portion conveys that care and quality were elevated over quantity and that guests should eat more slowly to savor and enjoy. It also leaves room for appetizers and desserts.

Ways to make a plate look better:

vary plate shapes

use complementary colors

paint the sauce

design the negatie space

bed it – put it on a bed of lettuce, rice, etc.

I highly recommend this book to anyone who wants to learn more about culinary facts!

I look forward to reading, learning, and sharing more with you soon!

My intention is to post a Thoughtful Thursday column each week and share some of the insights I have learned in the past week. Here are some of the things I’ve learned this week:

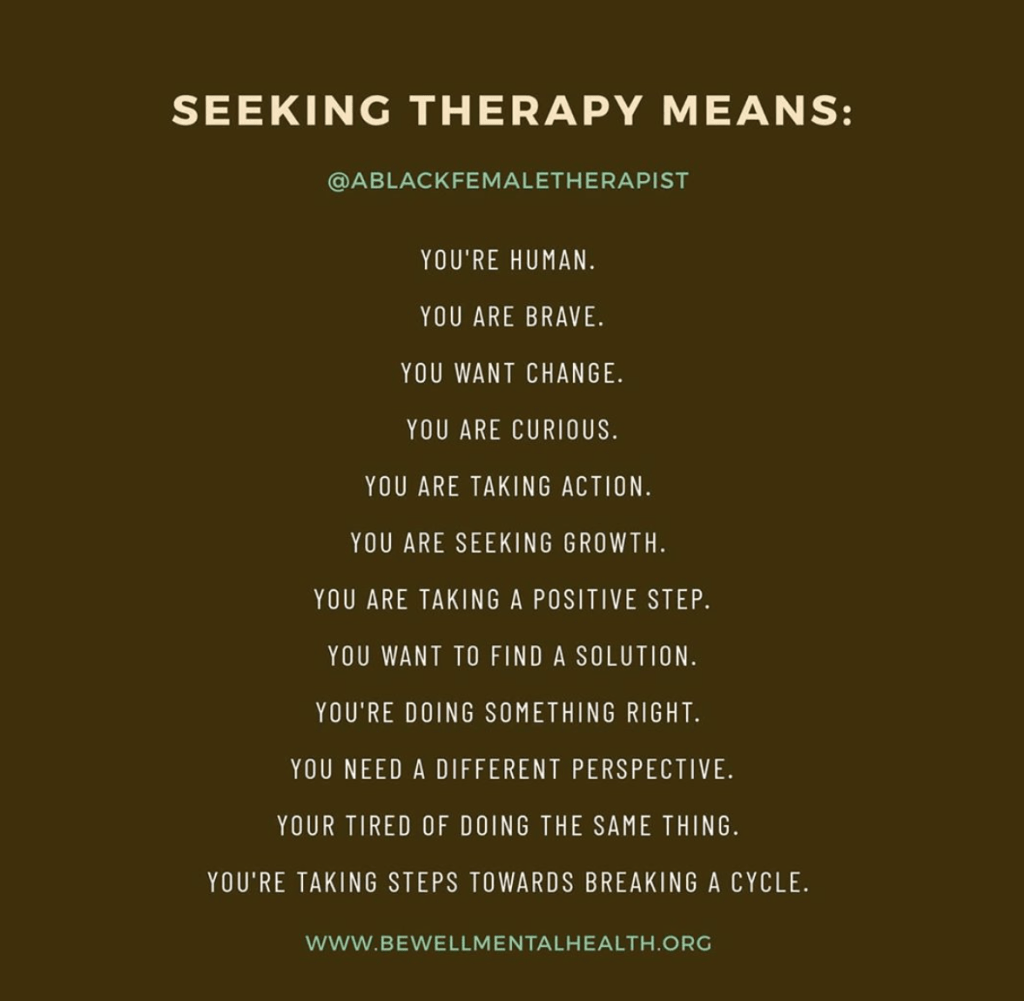

Optimal Living Daily – 10 Reasons You Would Benefit From Therapy

You feel betrayed by your romantic partner.

You feel betrayed by whatever success you have attained.

You feel betrayed by your job that has become uninteresting, stupid, and boring.

You feel betrayed by your coworkers and business associates who now seem to take more pleasure in your failures than your triumphs.

You feel betrayed by your body.

You feel betrayed by your health.

You feel betrayed by your government.

You feel betrayed by your friends and family members.

You feel betrayed by your parents for loving you conditionally.

On the cognitive level, a therapist can provide fresh perspectives and help you reframe your current situation so that you can either make immediate changes or accept your state of affairs.

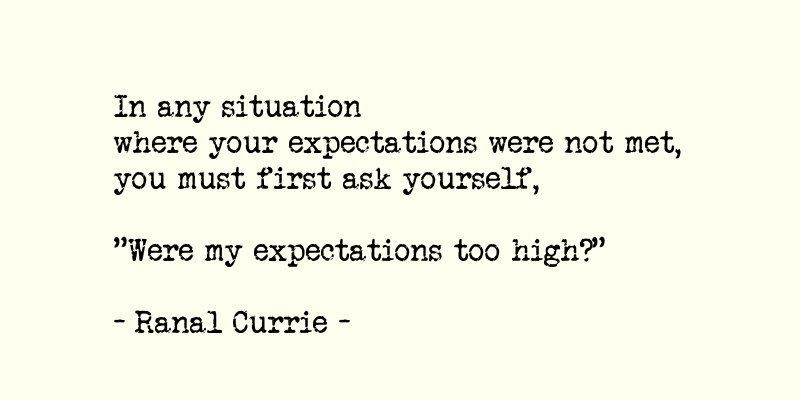

This post from Seth’s Blog this week was a great reminder about setting higher expectations for those you trust:

“When we raise our expectations for a student, a friend or a co-worker, we open the door to possibility. We offer them dignity and a chance to grow. We are offering them trust.

But if we become attached to those expectations, if the expectation unmet leads us to distress or unhappiness, then that attachment undermines the very reason we created the expectation in the first place.”

Inside Out Money – Reflections on one year of early retirement

If you want an extraordinary life, you must build it. Noone is handing out extraordinary lives.

ON SUCCESSS:

In retirement, no one is measuring your success except for yourself. There won’t be an annual performance review.

New challenges can be projects and not a means to make money.

ON STRUCTURE:

“For your entire life, much of your life was dictated by some kind of authority or schedule you didn’t create. When we have full autonomy over our time, many of us find this disorienting.”

“I miss the structure work provided and the feeling of doing something productive and constructive, but I don’t miss work.” “I feel like I’m able to be myself more.”

“I feel less stressed from not working. With less stress, I am able to be more physically and emotionally present.”

ON STRESS:

“I still take on too much and burn myself out. These are personality traits.”

“I still find things to stress about and be anxious about. I still procrastinate more than I should. I still deal with analysis paralysis. These are part of my personality.”

ON TIME:

“I am still trying to figure out how to spend my time intentionally and what I want to do with my time.”

“I want to spend more time on myself and the things I want to do.“

“I have spent too much of my first year like I have spent the last twenty years. I am doing too much for other people and doing too much to feel accomplished.”

ON LIVING YOUR BEST LIFE:

“I need to make some very thoughtful and active changes to make the life I want to be living.”

Many people think that when they retire and have the time, they will be living their best life. Just having time alone is not going to fix that. You can fill your time with all kinds of things, but it takes deliberate work and action, and you must be intentional about using your time. Having more time will not automatically change you and change all of your bad habits or make you live your best life.

ON EXPENSES:

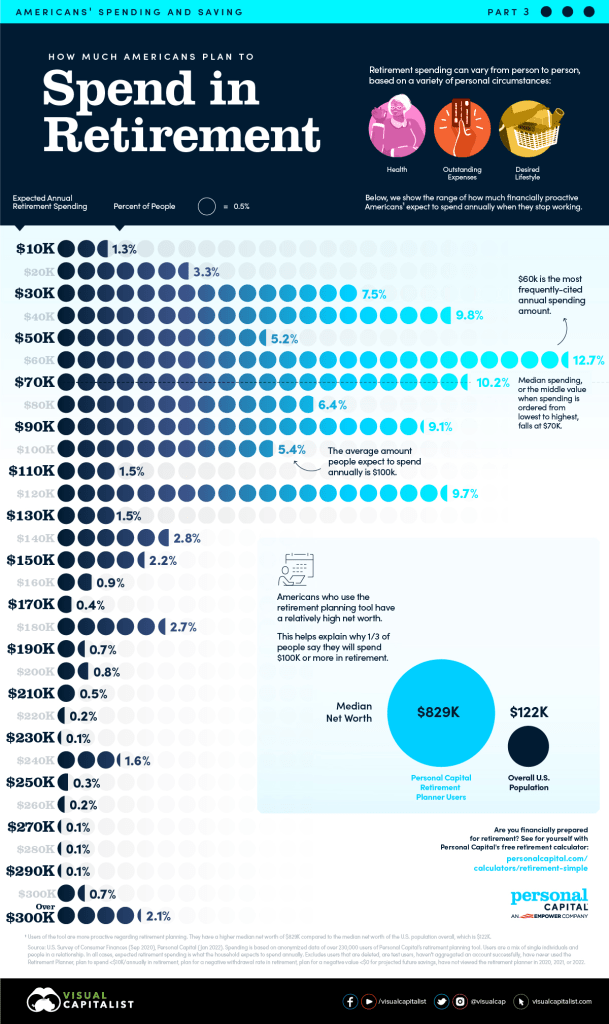

“Our expenses were more than expected our first year in early retirement due to travel and health insurance/health expenses.”

More time on your hands can easily result in spending more money. People sometimes spend more money when they are retired.

“Our overall net worth has increased since retiring last year due to investments performing well.”

Auto insurance:

liability insurance – covers you when you are responsible for others’ injuries or property damage that you cause with your car. It only pays up to maximum limits covered in your policy. You are responsible for paying the amount over the limit out of your own pocket.

Comprehensive and collision insurance – often come as a package deal – insurance pays to fix or replace your car after it’s damaged, even if the damage was your fault. Collision and comprehensive coverage often come with a deductible – the amount you pay before your insurance provides coverage. Ex: $500 to $2000

Insurance companies only pay UP TO the fair-market value of your car. If you drive an older car and have plenty of cash on hand to repair or replace it if you have to, you probably don’t need to have comprehensive and collision insurance. However, lenders and lessors require you to have this coverage if you are financing your car.

Uninsured/underinsured motorist coverage – often a package deal – your insurance pays you for medical expenses or damage to property caused by a driver who is uninsured or underinsured. It’s like a reverse liability insurance.

20 states require drivers to have this coverage. Some estimates are that 1 out of 8 drivers don’t have insurance!

Outside what your state requires you to have, ask yourself: Can you afford to pay out of pocket if your car gets badly damaged or stolen? If not, consider collision and comprehensive coverage. Do you drive a lot/are the roads very busy? If so, the risk of getting in an accident is higher, so you will want liability and uninsured/underinsured motorist coverage. Who’s on your policy? If you have young drivers, get better coverage due to the risk of accidents.

If you buy the cheapest car insurance, you’re basically buying your state’s bare minimum coverage to drive. If you get in an accident, you will likely need to pay a lot of money to cover what your insurance doesn’t. Cost can really stack up in nightmare scenarios.

Car insurance can be expensive. The average cost of minimum coverage for a good driver with good credit is $57/month. Full-coverage insurance costs about $180/month, on average.

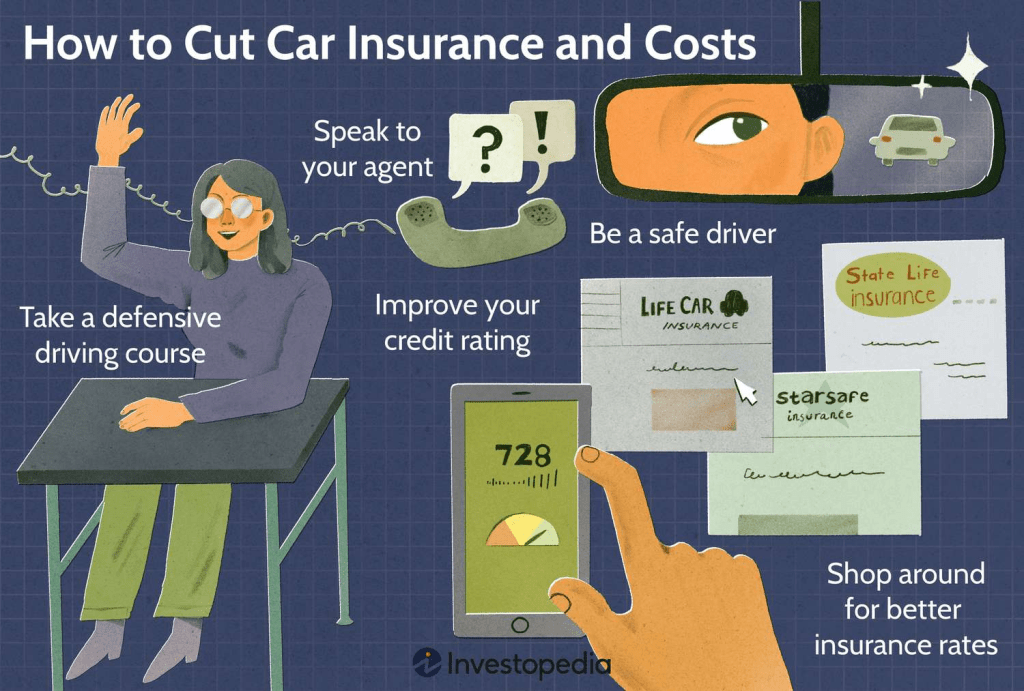

Car insurance rates have gone up 19% in the past year. Save money on insurance by shopping around. Only about ¼ of customers shop around at least once a year!

Ask your insurance company about discounts. You can get discounts for being a good driver, paying a policy in full, not driving much, etc. You can also raise your deductible to save on costs. You just need to make sure you have the cash on hand to cover the deductible. Make sure you aren’t paying for coverage you don’t need; if you have an older car, you might be able to drop comprehensive and collision insurance. If you have several vehicles, you could drop rental car reimbursement coverage.

There are several different factors that go into pricing policies: your driving record, your age, where you live, your credit score, etc.

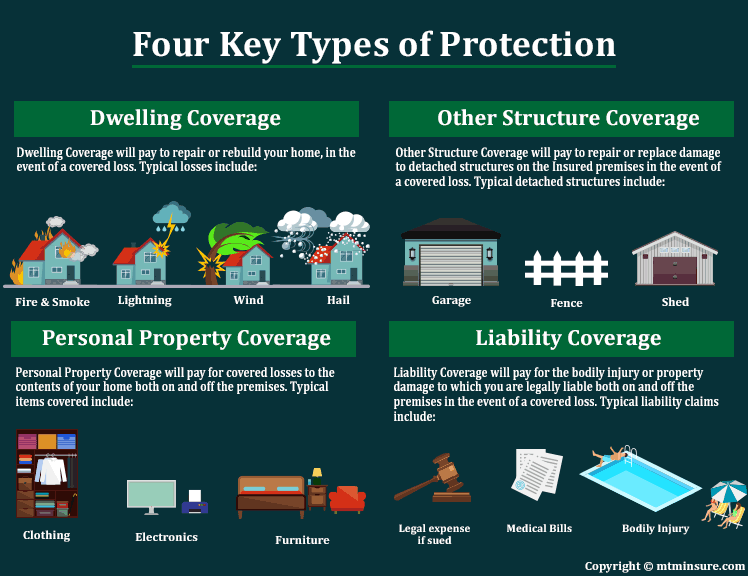

Home insurance:

dwelling coverage – typically pays for damages caused by sudden or accidental events only, not things that happened slowly over time or that you could have prevented through maintenance. Floods and earthquakes are often excluded from normal dwelling coverage unless you purchased those coverages.

Dwelling insurance matches the replacement cost of your home and attached structures – if you had to rebuild your home from scratch. Make sure your dwelling coverage is keeping up with inflation and rising building costs by checking with your insurance company from time to time. Also, keep them updated of any major renovations, such as a kitchen. For a more hands-off approach, you can add an inflation-guard to your policy to adjust your coverage automatically to keep up with inflation. Many people are underinsured and find out when it’s too late.

Personal property insurance – will pay to replace the stuff you own if it’s stolen or destroyed. Your belongings are typically covered only if you name them specifically in your policy! Your coverage may have special limits on items, such as jewelry and firearms.

Personal liability coverage – covers injuries on or off your property/damage you accidentally cause to someone’s stuff. Ex: if your dog bites someone, someone trips on your pool deck, etc. It only pays up to a certain limit, which you can increase or decrease.

Loss of use coverage – pays for living expenses if your home is unlivable and being repaired after a covered loss, like a fire. It pays for hotel expenses, food, storage costs, etc. It only pays for you to maintain your normal standard of living.

12% of Americans don’t have homeowners insurance! Homeowners insurance is required if you have a mortgage.

Insurance companies are losing money and increasing rates.

Shopping for car and home insurance can become fun to save money and compare rates. The internet makes things easier to compare rates, but when you compare rates, try to compare similar coverage amounts. If you don’t want to do the legwork yourself, you can use a broker. Some brokers require a small fee for their help.

One of the books I read in the past week is “101 Things I Learned in Culinary School” by Louis Eguaras with Matthew Frederick. Here are some of the most interesting things I learned. I will share more in a future blog post.

“Guests seek more from a dining experience than to satisfy their appetites: comfort, prestige, value, relaxation, artistry, social fun, or perhaps just a good place to watch the game. Be clear why customers choose your restaurant. Prioritize what they most need.”

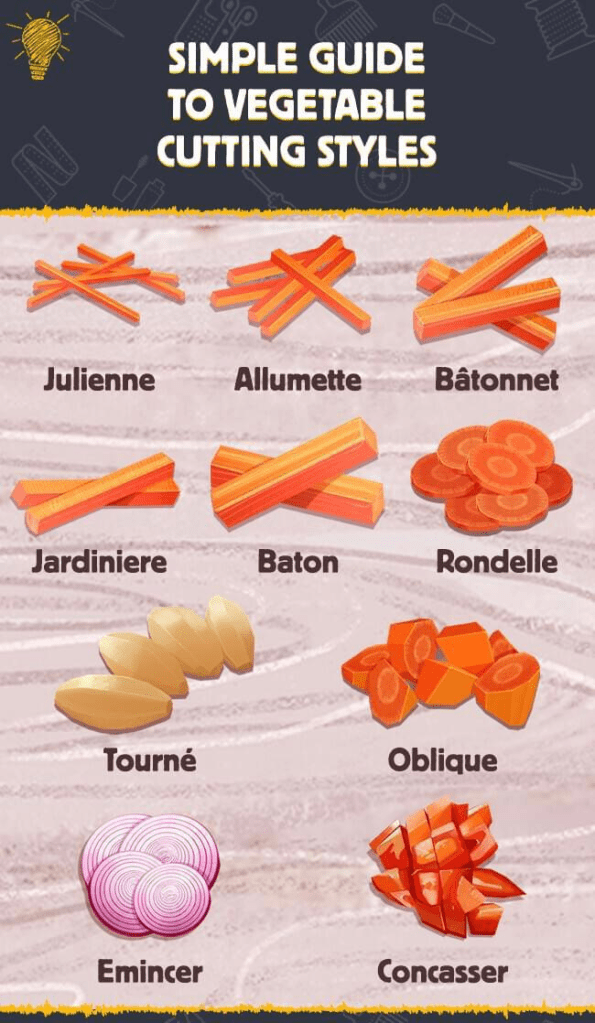

Knife cuts:

School teaches you how to cook. Experience teaches you how to be a chef. A cook follows a recipe; a chef can intuitively modify a recipe. A cook knows how; a chef knows why.

A pepper’s name often changes when dried.

I look forward to reading, learning, and sharing more with you soon!